Doing Business in Brazil: 6 Key Legal Points to Consider

1. Types of Company

Foreign investors wishing to incorporate a company in Brazil generally choose between the sociedade limitada and the sociedade anĂ´nima.

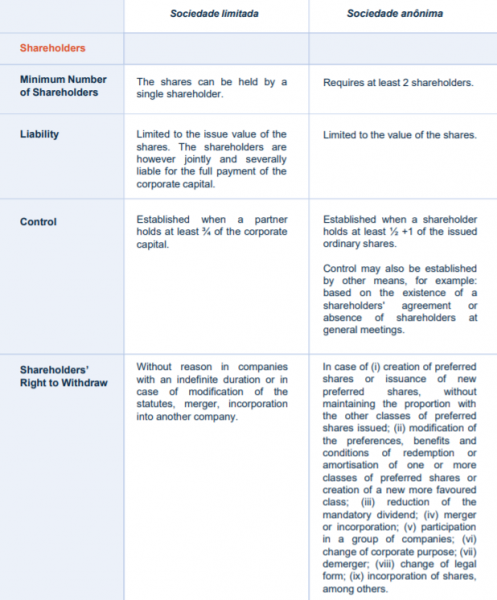

I. The Sociedade Limitada

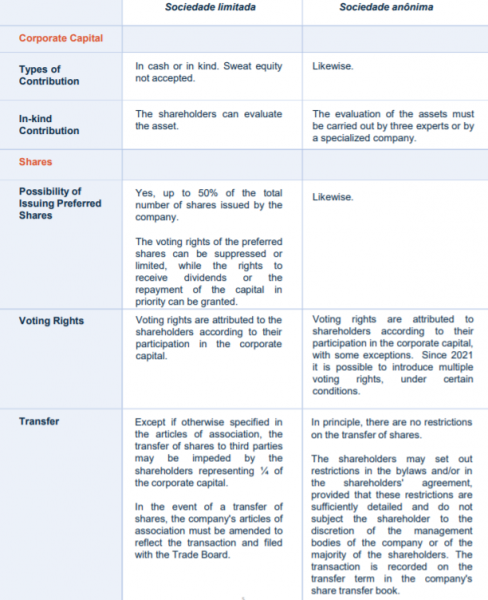

The sociedade limitada is the preferred type of company for most foreign investors because of its greater flexibility and simpler formalities. The corporate capital is divided into shares that can be held by foreign persons or entities, and the liability of each shareholder, vis-à -vis third parties, is limited to the value of the shares held.The control of the company is exercised by the holders of ž of the corporate capital, but certain matters may be approved by the shareholders holding a majority of the corporate capital or a majority of those present at the shareholders' meeting. While sweat equity is not allowed, in-kind contributions are possible if the value of the contributed property is approved by the shareholders. Since 2019, it is possible for a sociedade limitada to have only one shareholder.It should be noted, however, that the sociedade limitada is not an ideal instrument for attracting investments, because, inter alia, of (i) the rule that provides for joint and several liability of the shareholder for the payment of the corporate capital and (ii) the less favourable tax treatment regarding the taxation of goodwill in capital increase/fundraising operations.

II. The Sociedade AnĂ´nima

The ownership of a sociedade anĂ´nima is divided into shares and the liability of each shareholder vis-Ă -vis third parties is limited to the issue value of the shares held. While sweat equity is not allowed, in-kind contributions are possible but require the prior evaluation of the property by Three experts or by a specialized company.There must be at least two shareholders.General meetings may validly deliberate, on first call, with the presence of shareholders representing at least Âź of the shares with voting rights and, on second call, with the number of shareholders present. As a rule, decisions are taken by an absolute majority of votes.

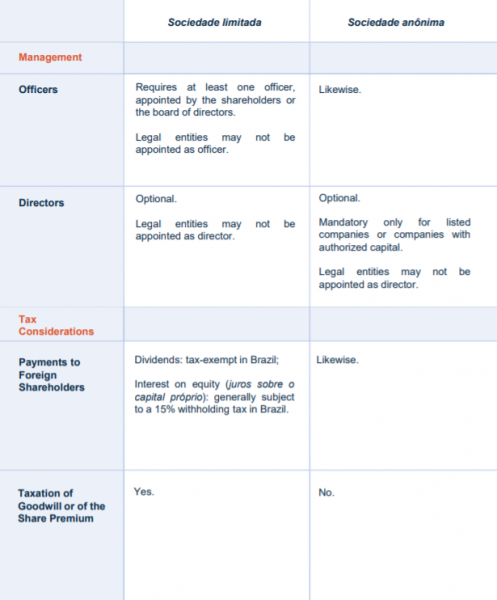

2. Representation of the Shareholders and Administration of the Company

Foreign shareholders of a Brazilian subsidiary (either an individual or a legal entity) must appoint a local representative with the necessary powers to represent them and to receive judicial acts. This legal representative does not have to be Brazilian. However, if the legal representative is a foreigner, he or she must reside in Brazil and be in possession of a visa.Regardless of the type of company, the officers must necessarily be natural persons and do not need to be domiciled in Brazil.However, if the officer resides abroad, she/he will also have to appoint a local representative with the above-mentioned powers for a period of at least 3 years from the date on which her/his mandate ends.

3. Taxation

The Brazilian tax system is relatively complex and the assistance of a specialist in the matter is strongly recommended from the outset of the project.For example, regarding income tax, except for specific cases provided by law, any company may choose, at the beginning of each year, the tax regime applicable to its activity. This choice will have implications on several points, such as the amount of taxes paid and their basis.There are two main tax regime options: lucro presumido (presumed profit) and lucro real (real profit).Lucro presumido (presumed profit): Under the presumed profit regime, taxes are levied on the companyâs monthly declared revenues pursuant to a profit margin âpresumedâ by law. Consequently, a companyâs actual costs and expenses do not reduce the taxable basis under this tax regime.Depending on the companyâs activities, the âpresumed marginsâ vary from 8% to 32%. From a tax perspective, the presumed profit regime may be more tax efficient in the case of companies with high profit margins (e.g., higher margins than the ones set forth in the legislation).The regime is eligible for companies with annual gross revenues of up to 78 million reais. Certain Brazilian companies, such as financial institutions, companies that generate profits, income or capital gains in foreign countries or companies subject to income tax benefits are not permitted to elect the presumed profit tax regime and are thus obliged to elect the real profit regime.Lucro real (real profit): Under the real profit regime, taxes are levied proportionally to the companyâs profit, calculated based on book results before taxes, adjusted by certain additions and deductions as set by the legislation. Tax losses may be carried forward to the following years without time restrictions. Yet, losses from previous years may be deducted from the companyâs profits in any given year only up to a limit of 30% of the yearly profit.Consequently, the real profit regime is more beneficial for companies operating with a loss or with lower profit margins. Oftentimes, international businesses setting up their Brazilian operations will in a first moment incur higher expenses and, therefore, elect to be taxed under the real profit regime.

4. Intellectual Property

It is strongly recommended to register the company's intellectual property with the National Institute of Industrial Property (INPI) in Brazil. The latter is competent for the registration of the following intelectual property rights: trademarks, patents, designs, geographical indications, and software.The use of intellectual property rights by the Brazilian subsidiary may, if applicable, generate royalties for the parent company. A thorough tax analysis of the transaction would be advisable.

5. Reporting Requirements to the Brazilian Central Bank and Register of Beneficial Owners

Any Brazilian company that receives funds from abroad, either through a capital contributions or by means of a loan agreement, or that has a foreign shareholder, must systematically report those activities to the Brazilian Central Bank. Brazilian companies are also required to register beneficial owners. According to Brazilian law, a beneficial owner is the natural person who, directly or indirectly, holds more than 25% of the corporate capital of the company or group of companies in question or has the power to make decisions in the company's deliberations and to appoint the majority of the company's officers.Among the companies exempt from fulfilling this obligation are those whose shares are listed on the stock exchange, in Brazil or abroad.

6. Accounting

Brazilian companies are required to use the services of an accountant. Brazil adopts IFRS (International Financial Reporting Standards), with some adaptations.A simplified version of IFRS may be adopted by any Brazilian company, except in one of the following cases:⢠A company whose total assets exceed R$ 240,000,000.00 or whose annual gross income exceeds R$ 300,000,000.00 or whose group of companies meets any of the above conditions;⢠A listed company; or⢠A company regulated by the Central Bank of Brazil, the Superintendence of Private Insurance or any regulatory body with regulatory authority (e.g., one of the many national agencies in Brazil: National Telecommunications Agency, National Health Surveillance Agency, etc.).

|